Car insurance used to feel pretty straightforward: you bought a six-month or twelve-month policy, paid the bill, and moved on. But lately, more drivers are asking a different kind of question: What if I only need coverage for a short time? Or, what if I need insurance now but can’t handle a big upfront payment?

That’s where flexible car insurance options come into the conversation. Between rising premiums, changing work schedules, borrowed vehicles, seasonal driving, and people moving between states, drivers are looking for coverage that fits real life instead of forcing them into a one-size-fits-all setup.

To be clear, flexibility does not mean skipping proper coverage or choosing the first cheap option that appears online. It means understanding what kind of policy you actually need, comparing your options carefully, and making sure you meet your state’s insurance requirements.

Why Drivers Are Looking for More Flexible Coverage

For many people, the biggest issue is cost. Car insurance premiums have become a bigger part of the monthly budget, especially for drivers who already have rent, groceries, fuel, repairs, and loan payments to think about. When a policy requires a large down payment before coverage starts, that can be a real problem.

Some drivers are also dealing with temporary situations. Maybe they borrowed a car for a few weeks. Maybe they are visiting family in another state. Maybe they just bought a vehicle and need coverage while deciding on a long-term policy. Others may only drive during certain seasons or need insurance while between standard policies.

In these cases, traditional auto insurance may still be the right answer, but drivers often want to know whether there are more practical ways to start coverage without overcommitting or overpaying upfront.

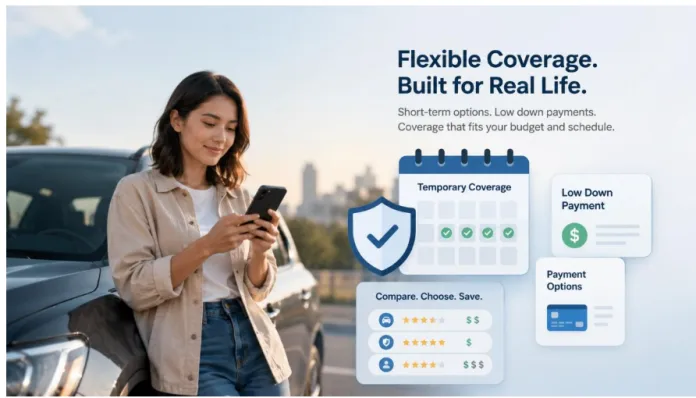

What Temporary Car Insurance Usually Means

Temporary car insurance sounds simple, but it can mean different things depending on the situation. In many states, major insurers may not sell a policy labeled exactly as “one-day” or “weekly” car insurance. Instead, short-term needs are often handled through regular policies that can be canceled later, non-owner policies, rental car coverage, permissive-use rules, or specialized arrangements depending on the driver and vehicle.

That’s why it is important not to assume every short-term option works the same way. A person borrowing a friend’s car may have different needs than someone renting a vehicle, buying a used car, or driving for a few months while temporarily living in another state.

For example, drivers researching short-term options in Georgia may find comparison resources discussing temporary car insurance in Georgia helpful as a starting point. The key is to use those resources to compare possible paths, understand common coverage situations, and then confirm the details before choosing a policy.

Low Down Payment Policies Are a Different Type of Flexibility

Temporary coverage is about how long you need insurance. Low down payment car insurance is usually about how much you need to pay upfront to begin coverage.

This matters because many drivers are not trying to avoid insurance. They are trying to avoid a large first payment. A policy may have a reasonable monthly rate, but the initial cost can still be hard to manage if the insurer asks for a big percentage of the premium upfront.

That’s why some shoppers look for policies advertised with smaller starting payments. When researching this topic, a comparison page about $20 down payment car insurance can help drivers understand how these low-upfront-payment options are commonly discussed and compared online.

Still, it is worth paying close attention to the full cost. A smaller down payment does not always mean the cheapest policy overall. Sometimes the monthly payments are higher, or fees may be added. The smartest move is to compare the total premium, payment schedule, cancellation terms, and coverage limits — not just the first payment.

The Cheapest Option Is Not Always the Best Option

It is completely normal to want cheaper car insurance. Nobody wants to pay more than necessary. But choosing based only on price can backfire if the policy does not provide enough protection.

Minimum liability coverage may satisfy state law, but it might not be enough if a serious accident happens. Full coverage can cost more, but it may be important for financed vehicles or newer cars. Some drivers may also need uninsured motorist coverage, roadside assistance, rental reimbursement, or other add-ons depending on their situation.

The best policy is usually the one that balances affordability with realistic protection. A low upfront payment can be useful, and temporary coverage can solve a short-term problem, but the coverage still has to make sense for the driver’s actual risk.

State Rules Can Make a Big Difference

Car insurance is regulated at the state level, so what works in one place may not work the same way somewhere else. Minimum coverage requirements, cancellation rules, proof-of-insurance standards, and available policy types can vary.

That is especially important for drivers who recently moved, students living away from home, people working temporarily in another state, or anyone buying a car outside their home state. A policy that seems fine in one location may not satisfy the rules in another.

Before buying anything, drivers should check the minimum insurance requirements in their state and ask how the policy handles their specific situation. It is also smart to confirm whether coverage starts immediately, whether proof of insurance is available right away, and what happens if the policy is canceled early.

When Flexible Coverage Can Make Sense

Flexible car insurance options may be worth looking into when a driver needs coverage quickly, has a limited budget for the first payment, or only needs insurance for a specific period. These situations can include borrowing a car, buying a car, replacing a canceled policy, driving temporarily in another state, or managing a tight month financially.

But flexibility should not be confused with shortcuts. Drivers still need valid insurance, accurate information on the application, and enough coverage to protect themselves from major financial trouble.

A good rule of thumb is to slow down just enough to compare. Look at several quotes, review the payment terms, check the coverage limits, and read the cancellation policy. Even a few extra minutes of comparison can prevent an expensive mistake later.

The Bottom Line

As car insurance costs continue to pressure household budgets, it makes sense that more drivers are asking about temporary coverage and low down payment options. People want policies that fit their lives, not just standard packages that assume everyone has the same budget and driving habits.

The good news is that comparison resources can make the process easier. They can help drivers understand common options, compare different approaches, and learn what questions to ask before buying coverage.

Whether someone is looking for short-term protection, a smaller first payment, or simply a more manageable way to stay insured, the goal should be the same: get legal, reliable coverage at a price that makes sense — without rushing into a policy just because it looks cheap at first glance.

References & Sources

This article has been fact-checked and verified against multiple public sources, financial disclosures, SEC filings, Forbes reports, Celebrity Net Worth databases, and official records. All net worth estimates are based on publicly available information and financial analysis.